We look forward to talking with with you. Contact us today!

Partner With PlanPerfect

We look forward to talking with with you. Contact us today!

Plans

Cash Balance Pension Plans

What is a Cash Balance Plan?

A cash balance plan (a “CB plan”) is a hybrid type of retirement plan that combines features of both pension plans and defined contribution plans (like a 401(k) plan or profit sharing plan). Like a defined contribution plan, each participant earns an “account balance”, but unlike most defined contribution plans, the earnings rate on the account is guaranteed for the participant. In addition, because the CB plan is a pension plan under the tax code, the limits on how much is added to the cash balance account can be significantly higher.

What are some benefits of a cash balance plan?

Benefits may accrue rapidly, allowing an owner to “catch up” when getting closer to retirement.

Higher limits on tax-deductible contributions than 401(k) plans.

The benefits in most CB plans are protected from creditors and may be guaranteed (with limitations) by the Pension Benefit Guarantee Corporation.

Plan investments can be professionally managed as one pooled balance.

Provides a valuable benefit to help attract and retain talent in a competitive marketplace.

Easy for participants to understand and value because the benefit is stated as an account balance.

Plans typically permit participants to take a lump sum, which the participant can roll over into an IRA or to another employer’s plan.

The earnings on plan assets can reduce future employer contributions.

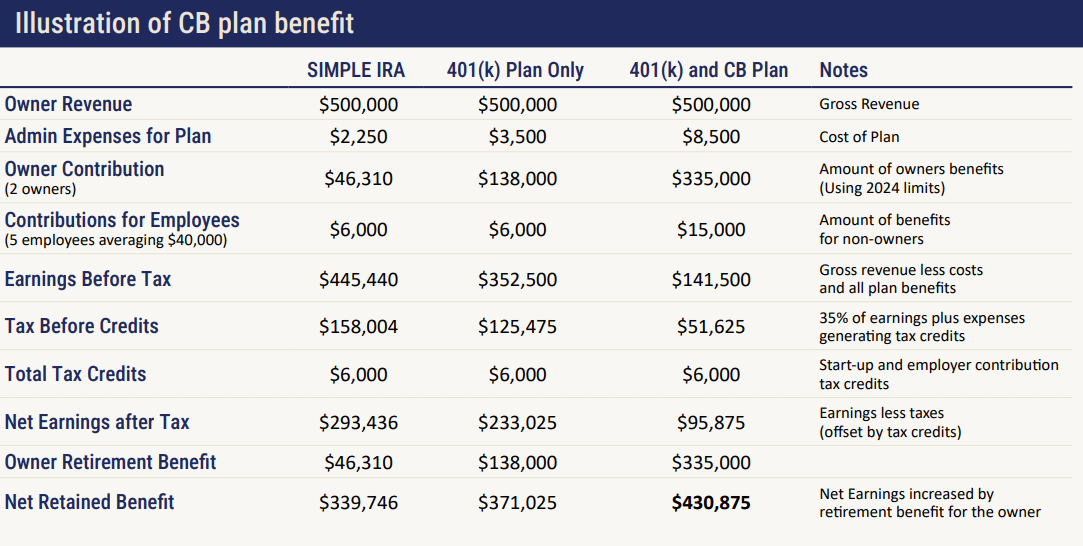

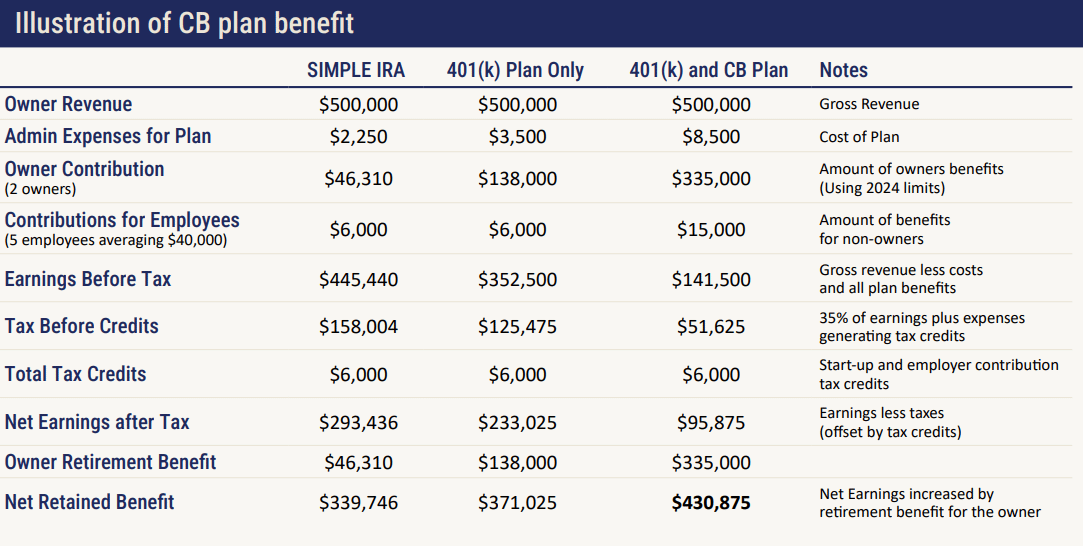

Owners with steady income may realize meaningful benefits from having both a CB Plan and a 401(k) plan. Owners may save more for retirement, and the tax savings can more than offset the additional expense. In addition, the more generous benefits for employees may be a significant tool to attract and retain a valuable workforce.

IMPORTANT ELEMENTS IN DECISION:

CB plans allow owners to save significantly more for retirement

CB plans require funding over several years, so steady revenue is necessary

How do Cash Balance Plans differ from 401(k) plans?

Participants typically are not required (or allowed) to contribute their own pay to the CB plan. Rather, eligible employees will earn benefits automatically.

The maximum benefit permitted by the tax code is calculated differently and, depending on age, may permit higher levels of benefits to accrue under the CB plan for a certain period of time.

The “accounts” under the CB plan are bookkeeping accounts—the plan assets are not segregated for each participant. The accounts

have a guaranteed rate of return for participants.

The company is responsible for making contributions and investing those assets to ensure the plan assets are sufficient to pay all benefits. The company may be required to make certain levels of contributions depending on the plan’s funding status.

While most CB plans provide lump sums, which are the most popular distribution option for participants, the plan must also provide certain annuity distribution options.

Benefits may be guaranteed by the Pension Benefit Guaranty Corporation (PBGC).

What are some downsides to having a Cash Balance Plan?

The administration cost of the plan is usually higher because of the need for actuarial services, more experienced service providers, and PBGC premiums.

Nondiscrimination testing generally is required to be performed every year.

Contributions are required for a number of years, even if the amount of benefits is frozen in the future.

Required contribution amounts can fluctuate and may increase if the plan assets perform poorly. If contributions are required, the amounts will be owed even if the company is underperforming.

The investment risks are borne solely by the company.