We look forward to talking with with you. Contact us today!

Partner With PlanPerfect

We look forward to talking with with you. Contact us today!

Plans

What is Compensation?

COMPENSATION GUIDE

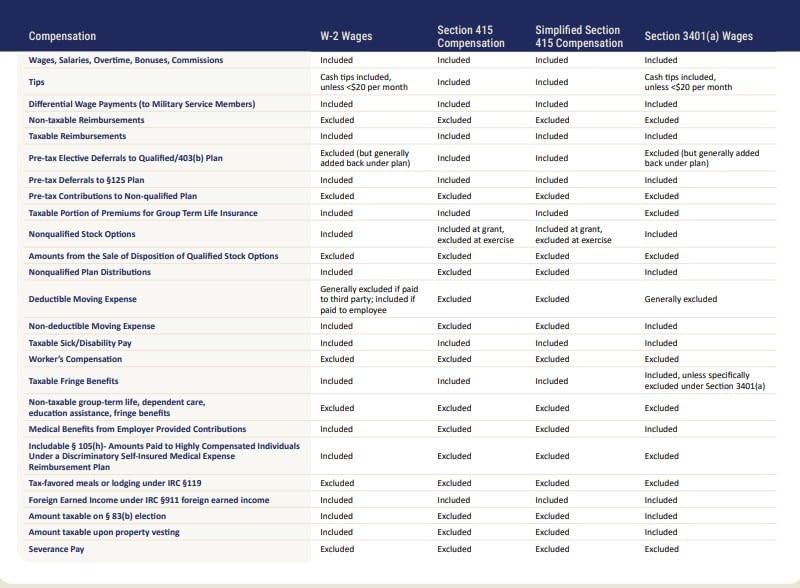

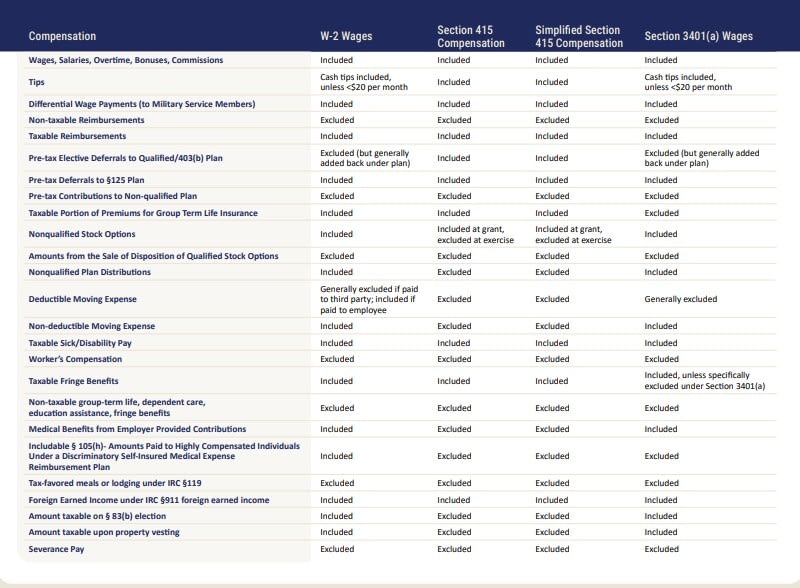

This guide is intended as a quick reference summarizing the four widely used definitions of compensation in plan design:

W-2 Wages

The amount of compensation listed on a participant’s W-2 in Box 1 (“Wages, tips, other compensation”). Generally, this includes all earnings, minus pre-tax retirement and benefit deductions, plus taxable benefits.

Section 415 Compensation

Generally, this includes all taxable compensation (e.g., salary, bonuses, commissions) and excludes items not currently included in taxable income (e.g., nontaxable fringe benefits, worker’s compensation, and nontaxable group term life insurance).

Simplified Section 415 Compensation

This is generally identical to Section 415 Compensation, though it excludes certain types of compensation that are often reserved for highly compensated employees (e.g., taxable moving expense reimbursements and nonqualified deferred compensation).

Section 3401(a) Wages

Generally, this includes all wages within the meaning of Code Section 3401(a), plus amounts that would be included in wages but for an election under Code Section 125(a), 132(f)(4), 402(e)(3), 402(h)(1)(B), 402(k), or 457(b).

Compensation of Owners

Note that owners who are considered

“self-employed” under the tax code

generally will have compensation

based on earned income.

Sole Proprietor

Earned Income

Partner

Earned Income

S-Corp Owner

Plan definition; pass-through

income is not counted

C-Corp Owner

Plan definition; No pass-through

income

For limited liability entities (LLCs, LLPs, PLLCs, etc.) – the owners are treated in accordance with the entity’s tax election. For example, owner of an LLC that elects to be taxed as a partnership will be treated the same as partners.