We look forward to talking with with you. Contact us today!

Partner With PlanPerfect

We look forward to talking with with you. Contact us today!

Simple IRA to 401k

Converting a SIMPLE IRA to a Safe Harbor 401(k)

This guide is intended as a quick reference summarizing the provisions under SECURE 2.0 that permit plan sponsors to terminate a SIMPLE IRA mid-year and transition to a safe harbor 401(k) replacement plan.

What Changed

re: Converting a SIMPLE into a 401(k) Plan?

Before 2024 terminating a SIMPLE plan to start a 401(k) plan could only be done effective the first of the calendar year. Beginning January 1, 2024, plan sponsors may terminate a SIMPLE plan mid-year and replace it with a 401(k) plan as long as:

The replacement plan is a safe harbor 401(k) plan; and

Is established as of the day after termination date of a SIMPLE plan.

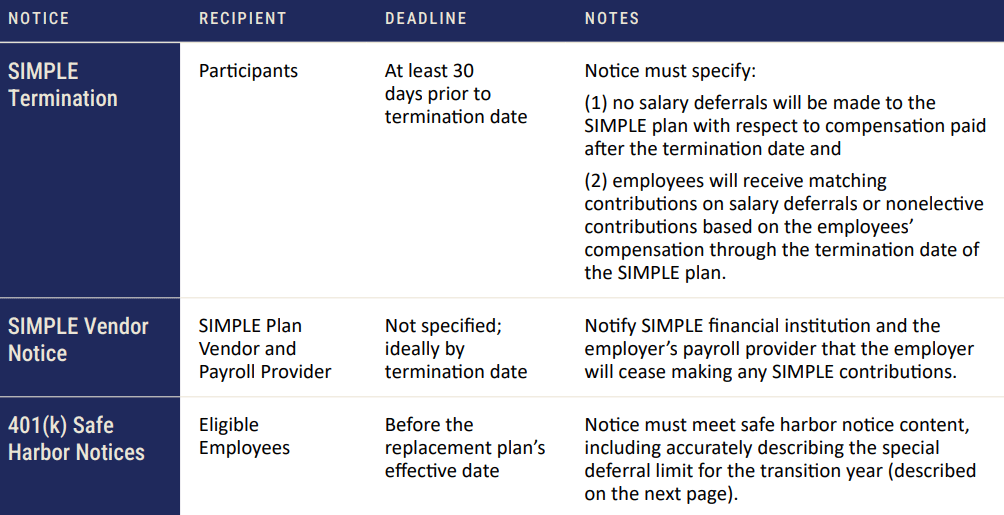

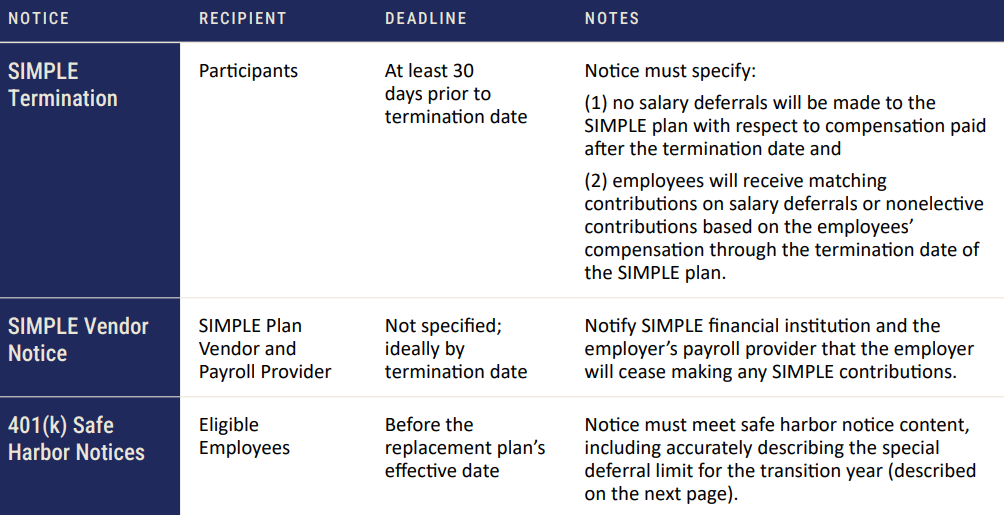

Notices and Whom to Contact

Certain notices are required in connection with the termination of the SIMPLE plan and establishment of the safe harbor 401(k) plan.

401(k) Plan Deferral Limits

For the transition year (during which the 401(k) plan is established), participants will not be allowed to make deferrals up to the full 402(g) limit. Rather, the deferral limit for the year will be a weighted average of the SIMPLE plan limits and 401(k) plan limits. Each participant’s total contributions between the SIMPLE and 401(k) cannot exceed this limit. If the participant is eligible for catch-up contributions, the available catch-up is also a weighted average. Calculation:

This results in the available deferrals to the 401(k) plan varying for each individual participant because the available limit depends on how much the employee contributed to the SIMPLE prior to termination. Individual calculation:

Distributions – Rollover Available

Typically, distributions from a SIMPLE IRA are not eligible for rollover if they are distributed within the first two years that a participant began participating in the SIMPLE IRA. If the SIMPLE is terminated (whether mid-year or not) and the employer replaces the plan with a 401(k) or 403(b) plan, then rollovers from the IRA to the 401(k) or 403(b) plan are not subject to the normal penalty as long as the rollover contributions are made subject to the replacement plan’s in-service and other withdrawal restrictions applicable to employee deferrals.

Tax Credits

Assuming the employer is an eligible small employer, tax

credits may be available as follows:

The start-up costs tax credit will not be available.

The employer contribution tax credit may be available beginning with the employer’s tax year after the tax year that includes the transition year, and

The tax credit for automatic contribution arrangements may be available.

Employers should always consult and rely upon tax advisors to confirm eligibility for tax credits.

Testing Issues: 415 Limits and Compensation Limits

No special rules or guidance have been issued on these issues. If the 415 limit year is the calendar year (not the plan year), then the full 415 limit should be available under the 401(k) plan for the transition year, even if the plan has a short plan year. If the first plan year for the 401(k) plan is a short plan year, then the 401(a)(17) compensation limit will be prorated to reflect the short plan year.

Checklist

1. Action to Terminate SIMPLE Plan:

Formal written action

Specifies the date as of which the SIMPLE is terminated

2. SIMPLE Contributions

No salary deferrals made for periods after the termination date

Employer contributions made with respect to periods prior to termination date